On Monday, the total return on Japanese government bonds of all maturities reached a six-month high. Japanese bonds suffered their worst sell-off in two decades.

Japanese bond yield:

In July this year, the ten-year Japanese bond yield fell to a record low of -0.291%. Later, due to market uncertainty about Japan's monetary policy, Japanese government bond yields fluctuated and retreated from the lowest point in July. The Japanese government announced a US$45 billion economic stimulus package in July, but the stimulus was lower than market expectations. The market is worried that the Bank of Japan's economic stimulus is insufficient, which further intensifies the selling of Japanese bonds.

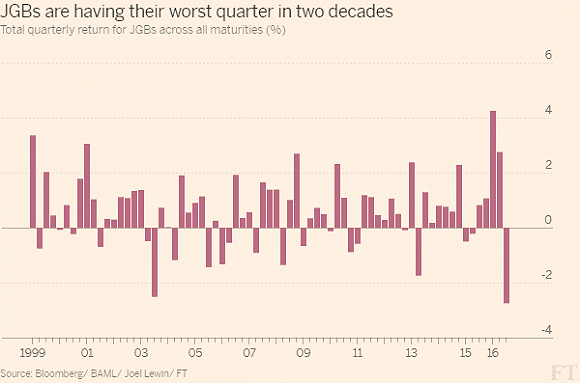

Merill Lynch Bank analyzed that the cumulative loss of Japanese bonds this quarter has reached 2.75%, which is the highest quarterly loss rate since 1998. The sell-off in long-dated Treasuries was even more ferocious. The quarterly loss for Treasury bonds with ten years or more was 5.9%, the worst loss in 13 years.

The Bank of Japan will make a public statement on its policy in the second half of the month. Yet the announcement risks further confusing the market. Investors expect the Bank of Japan's meeting next week to cut short- and medium-term bond yields while raising long-term bond yields. This steeper yield curve would give banks more room to improve their earnings. However, as the central bank meeting approaches, investors are panicking: Will the central bank further cut interest rates on the basis of negative interest rates?

Ken Takamiya, chief Japan bank analyst at Nomura Securities, believes there is nothing to fear except fear itself. He pointed out that cutting interest rates on top of negative interest rates will certainly not promote spending. He believes that even if the Bank of Japan cuts interest rates again, banks will find new ways to make profits. Banks are likely to adopt structural adjustments, such as reducing costs, widening lending spreads, and introducing account maintenance fees. The latter, in particular, may curtail the impact of negative interest rates.

Jefferies analyst Sean Darby and Northern Trust Capital Markets' Asia chief researcher Douglas Morton remain cautious about whether to buy bank stocks. Darby, an analyst at Mitsubishi Union Financial, pointed out this morning that the Bank of Japan may only buy long-term bonds, which would destroy investment opportunities for the private sector. At the same time, Douglas Morton is not optimistic about loan growth in the long term, and warned that bank stocks may not have bottomed out yet. “Due to the rebound in Japanese bond yields, Mitsubishi United Financial Holdings shares have risen 34% from their lowest point. However, this does not mean an increase in long-term borrowing, nor does it mean an end to the policy of negative interest rates. Although the current price-to-book ratio of the Japanese banking industry is only 0.5, in the context of the last Japanese financial crisis, we believe that bank profits are at risk of further decline. ”